Most AI startups are building in the wrong place. Not because they lack intelligence or resources — but because they haven't mapped the terrain clearly. The loudest quadrant in the room is rarely the one with the money.

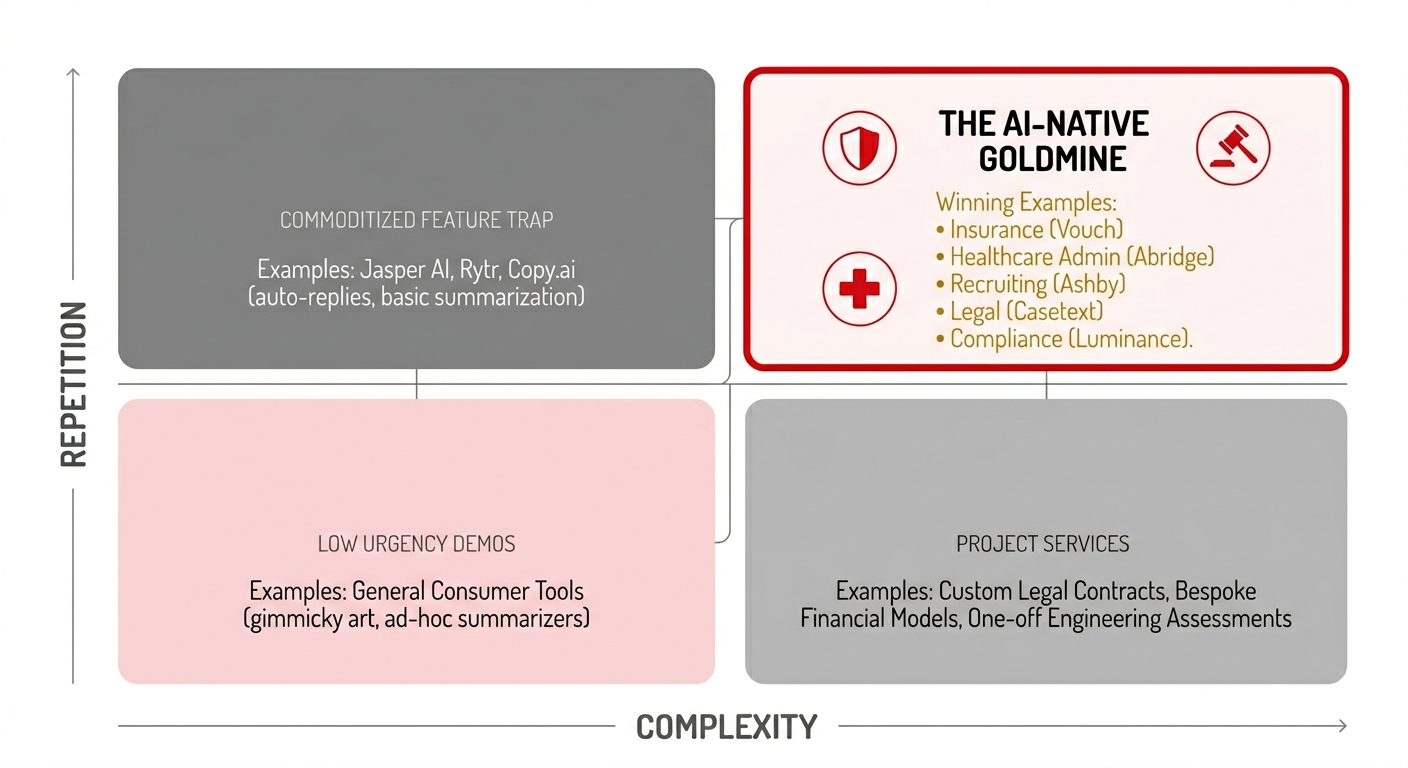

The AI Native Opportunity Map cuts through the noise with brutal simplicity: two axes, four quadrants, and one clear answer on where AI agents actually win.

The Two Axes That Actually Matter

The framework plots every potential AI-native workflow on two dimensions:

- Workflow Complexity (horizontal axis): How multi-step, conditional, and nuanced is the underlying process?

- Repetition (vertical axis): How frequently does this workflow recur — daily, weekly, hourly, at scale?

Every business problem you consider building an AI agent for falls somewhere on this grid. The problem is, most builders gravitate toward the quadrants that feel tractable — not the ones that are strategically defensible.

Mapping the Four Quadrants

Top Left — Too Simple, Already Commoditized

High repetition, low complexity. This is the most crowded quadrant. Think auto-replies, basic summarization, FAQ bots, and template generators. AI executes these tasks trivially, which means every incumbent SaaS vendor has already bolted them on as a feature. You are not building a company here — you are building a feature someone else will ship in Q3.

What happened here:

- Jasper AI is the cautionary tale. A few years ago, it was the poster child for generative AI success — fast growth, sleek UX, and a category-leading position in AI writing. Then GPT-4 and Claude became context-aware and style-adaptive, and Jasper's "custom tone" advantage evaporated overnight. The moat wasn't data or reasoning — it was just a model wrapper that any incumbent could replicate as a free feature.

- Rytr and Copy.ai face the same structural trap. Both pull from the same OpenAI engine as ChatGPT, leaving buyers asking the obvious question: why pay for a niche AI writing tool when ChatGPT does the same for less? Reviews highlight limited advanced features, output that requires heavy editing, and an inability to handle specialized or long-form content.

- The broader pattern is stark: 42% of startups fail because there is no market demand for their product, and rapid commoditization — when a new large model is released for free — makes previously defensible tools instantly irrelevant.

The switching cost is near zero. The moat is non-existent. Founders who land here are competing on distribution and pricing from day one, with no structural advantage.

Bottom Left — Not Painful Enough

Low repetition, low complexity. These are tasks that AI handles fine but that nobody desperately needs solved at scale. A workflow that happens once a quarter and takes 20 minutes does not justify a subscription, an integration, or a procurement cycle. Even if you build it beautifully, the pain tolerance of your buyer is too low to generate urgency.

What goes wrong here:

- Many consumer-facing AI startups fall into this trap — generative art tools, one-click presentation makers, and ad-hoc research summarizers that users love to demo but don't pay to retain. Several high-profile consumer AI products collapsed because users found them gimmicky or overpriced when the novelty wore off.

- The startup failure pattern here isn't a bad product — it's a bad problem. 34% of failed AI startups cite poor product-market fit as the primary culprit, and this quadrant is where most of that pain concentrates. Teams build technology first, then search for a market — discovering too late that the problem they solved wasn't painful enough to sustain a business.

This quadrant produces demos that impress and products that don't convert. Build here only if you're using it as a wedge into a more painful adjacent workflow.

Bottom Right — Complex but Not Repeatable

High complexity, low repetition. Custom legal contracts, bespoke financial models, complex one-off engineering assessments. These require deep reasoning but happen infrequently. AI can add real value here — but the revenue model is project-based, the sales cycle is long, and the margin compresses because customization costs dominate.

The reality check:

- Otter.ai started as a meeting transcription tool — a genuinely useful, AI-driven product. But transcription alone is a low-complexity, moderate-repetition workflow that was quickly matched by Zoom, Google Meet, and Microsoft Teams as a native feature. Otter has had to pivot repeatedly — now repositioning as an "Otter Meeting Agent" with CRM integrations and sales coaching to escape the commoditization trap.

- This is excellent territory for professional services firms augmenting their delivery. A boutique M&A law firm that uses AI to draft complex, one-off transaction agreements gains margin advantage — but that's not a scalable software business. It is not a repeatable AI-native product.

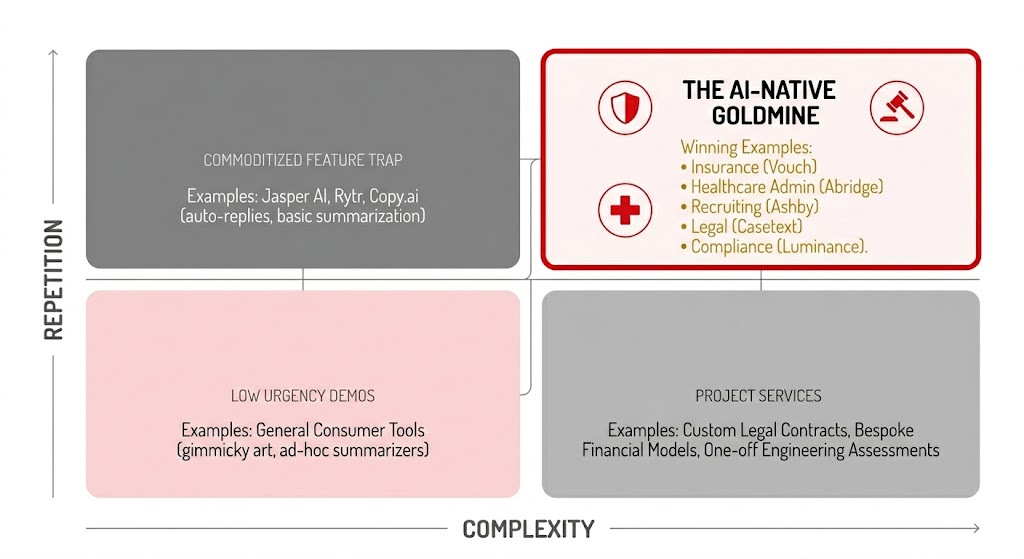

Top Right — The AI-Native Goldmine

High repetition, high complexity. This is where AI agents don't just assist — they replace entire operational roles. The AI agents market was valued at $7.84 billion in 2025 and is projected to reach $52.62 billion by 2030, growing at a 46.3% CAGR. The bulk of that value is being created right here.

Who Is Winning in the Goldmine — and Why

Insurance Operations

Insurance workflows are the definition of high-repetition, high-complexity. Claims triage, coverage verification, underwriting support, regulatory compliance — these run at scale every single day, governed by intricate rules, state regulations, and carrier-specific policies.

Vouch is a sharp example of a company that understood this structurally. Rather than building a generic insurance tool, Vouch became the dedicated AI-native insurance platform for startups — handling complex coverage decisions (E&O, cyber, AI liability) that repeat across every new customer they onboard. In 2023, they launched AI Insurance, a first-of-its-kind coverage for LLM hallucinations, algorithmic bias, and IP claims — a product that could only exist because the team was already embedded in a high-repetition insurance workflow. They raised $25M in a Series C-1 in 2024, reporting 66% year-over-year revenue growth.

The AI insurance market is projected to reach $4.7 billion in annual premiums by 2032, growing at an 80% CAGR — driven entirely by the complexity and frequency of regulatory and underwriting workflows that AI is uniquely positioned to handle.

Recruiting

Recruiting is operationally brutal at scale. Resume screening, candidate communication, interview scheduling, feedback synthesis, offer generation — these are complex, multi-step workflows that repeat hundreds of times per quarter in any growing company.

Ashby has become the fastest-growing ATS solution with over 4,000 active customers by deeply embedding AI across the entire recruiting stack — sourcing, scheduling, analytics, and CRM — rather than bolting it on as an afterthought. Companies like Multiverse switched to Ashby specifically to build a lean, data-driven recruiting operation that leverages AI at every stage.

Rippling took a different approach, integrating AI-driven candidate feedback summaries directly into its workforce management platform — so once a hiring decision is made, the ATS automatically syncs with HR, payroll, and onboarding in seconds. Leena AI goes further, operating as an autonomous HR agent that resolves 80% of helpdesk requests without human intervention, connected to 1,000+ enterprise applications.

These aren't AI copilots. They are AI operators, running the workflow start-to-finish.

Compliance

Compliance is the highest-stakes repetitive workflow in regulated industries. Financial services, healthcare, insurance, and legal sectors all run compliance checks daily — cross-referencing sanction lists, monitoring regulatory changes, flagging exceptions, generating audit trails. Failure is not just expensive; it is often existential.

Luminance built an AI compliance platform that automatically categorizes counterparties, runs parallel compliance checks (DORA, CCPA, sanctions), escalates flagged issues with AI-powered explanations, and continuously monitors existing relationships for emerging risks. This is not a chatbot. It is an operational compliance layer that runs in the background every day, on every contract, across the entire business.

Deloitte's analysis of AI compliance in insurance confirms the structural fit: AI offers insurers "a credible path to more effective and efficient compliance, particularly where traditional controls struggle" — delivering reduced false positives, faster cycle times, and stronger regulatory resilience.

Healthcare Administration

Healthcare admin is perhaps the most painful example of high-repetition, high-complexity work done almost entirely by humans under crushing time pressure. Prior authorizations, clinical documentation, billing reconciliation, HIPAA-compliant workflow management — these run in parallel across thousands of patient encounters per day.

Abridge is the clearest proof point. Its ambient listening AI attends doctor-patient conversations and automatically generates structured clinical notes integrated directly into Epic EHR. The results from real health system deployments are not incremental:

- 73% less after-hours documentation across UNC Health, Emory, KUMC, and Mayo Clinic

- Physician burnout dropped from 61% to 27.7% within 30 days of deployment at Riverside Health

- Providers save two hours per day on average — with deeply integrated EHR tools taking up to 75% less time to use than external apps

- KLAS rating of 95.3%, significantly above the industry average of 79.6%

Abridge became Epic's first AI partner in 2023 — a distribution moat that compounds every time a new health system deploys Epic across its hospitals.

Legal Intake and Research

Legal intake is a workflow that most law firms have never systematically automated — matter triage, conflict checks, document classification, research memo generation. These are complex, rule-dependent tasks that repeat across every new client engagement, every new matter, every day.

Casetext built CoCounsel, an AI legal assistant powered by GPT-4, that executes document review, legal research memos, deposition preparation, and contract analysis in minutes. The product served more than 10,000 law firms and corporate legal departments before Thomson Reuters acquired it for $650 million in cash in August 2023. That acquisition wasn't a talent buy — it was a recognition that Casetext had built a workflow layer so embedded in legal operations that it was worth nearly three-quarters of a billion dollars.

Harvey AI has continued that trajectory, hiring teams of former Big Law attorneys to sell AI workflows directly into law firms — understanding that domain expertise and sales credibility are as important as the model itself.

Emerging Goldmine Industries

The opportunity map extends well beyond the five sectors in the original framework. Any industry that shares the structural profile — high-repetition workflows with complex, conditional decision logic — is a target.

| Industry | Workflow | Why It's Goldmine |

|---|---|---|

| Supply Chain & Logistics | Procurement, inventory management, supplier risk monitoring | Multi-party coordination at daily volume; failures cascade immediately |

| Cybersecurity | Threat detection, alert triage, incident response | Thousands of signals per day, each requiring contextual reasoning |

| Financial Services | Fraud detection, loan processing, AML monitoring | Regulatory complexity + transaction volume = agent territory |

| HR & IT Helpdesk | Ticket resolution, onboarding, payroll reconciliation | Enterprise-scale repetition with multi-system conditional logic |

| Real Estate | Title search, contract review, compliance filing | High transaction volume, jurisdiction-specific rules |

| Education Admin | Enrollment processing, financial aid verification, regulatory reporting | Repetitive at institutional scale, highly rule-governed |

Vertical AI agents in these sectors are expected to grow at approximately 35% CAGR over the next five years, with vendors that combine proprietary domain data and deep workflow integration achieving the highest customer stickiness.

Why Agents Win in the Top Right

The argument is not just about automation. It's about where automation creates compounding structural advantage.

In high-repetition, high-complexity workflows, three things happen simultaneously when you deploy a capable AI agent:

- Speed collapses the bottleneck. Insurance intake that took 4 hours resolves in minutes. Recruiting screens 500 applications before a human drinks their morning coffee. Abridge saves physicians two hours per day — every day. The throughput advantage is measured in orders of magnitude, not percentage points.

- Consistency eliminates variance. Human operators in complex repetitive roles introduce error rates, mood-dependent quality, and training drift. An agent runs the same process the same way every time — this is regulatory gold in compliance and healthcare, where variance itself is a liability.

- Data compounds the moat. Every repetition generates labeled workflow data. Casetext's value to Thomson Reuters wasn't just its 104 employees — it was the corpus of legal workflows it had processed across 10,000 firms. The agent that has seen 100,000 claims, 500,000 resumes, or 1 million compliance checks understands edge cases that a new competitor cannot replicate without equivalent volume.

The Diagnostic Every Founder Should Run

Before committing to a roadmap, pressure-test your target workflow against both axes:

| Question | What a Strong Answer Looks Like |

|---|---|

| How often does this workflow run? | Daily or more — at per-seat or per-transaction volume |

| How many steps and decisions does it involve? | 5+ conditional decision points; domain knowledge required |

| What happens when it fails or slows? | Measurable operational cost — SLA breach, revenue delay, compliance risk |

| Who is currently doing this work? | A team of trained specialists following a documented process |

| What is the cost of doing nothing? | Growing headcount, increasing error rates, or customer attrition |

| Is there a data compounding effect? | Does processing more workflows make the agent smarter over time? |

If your target workflow scores high on every row, you are in the goldmine. If it scores low on repetition, reconsider whether you are building a product or a service. If it scores low on complexity, consider whether you are building a product or a commodity.

The Operator's Conclusion

The AI-native opportunity is real and large — and the evidence is in the exits, the funding rounds, and the retention metrics. Casetext at $650M. Vouch growing 66% year-over-year. Abridge achieving a 95.3% KLAS rating in a notoriously conservative buyer market. Leena AI resolving 80% of enterprise helpdesk tickets without human intervention.

The founders who will build durable companies in this cycle are those who resist the gravity of the easy quadrant — the one that's simple to demo, simple to explain, and simple to copy. The Jaspers and Rytrs of the world showed us what happens in the top-left: fast growth, then faster commoditization, then feature status on someone else's roadmap.

The money is in the workflows that are complex, repetitive, and operationally load-bearing. Insurance. Recruiting. Compliance. Healthcare admin. Legal intake. Supply chain. Fraud detection. These are not the flashiest verticals — but they are the ones where an AI agent becomes infrastructure, where pulling it out costs more than keeping it in, and where the switching cost is structural.

That is where agents win. That is where you should be building.